Introduction: The Hidden Value in Your Job Offer

For many professionals in Trinidad & Tobago, a good job is more than just a salary. One of the most valuable, yet often misunderstood, parts of any compensation package is the group health insurance Trinidad employers provide. It’s a fantastic benefit that offers a crucial layer of security for you and your family.

However, relying solely on your work plan without understanding its limitations can leave you dangerously exposed. Are you truly maximizing your benefits? And more importantly, is your employer-provided plan enough to weather a serious storm? Let’s break down how to get the most from your group plan and why a personal strategy is the key to truly comprehensive protection

Understanding Your Group Benefits: What to Look For

First, it’s essential to know what your group plan actually covers. Every plan is different, but you should look for these key components in your benefits booklet:

- Major Medical: This covers hospitalization, surgery, and significant medical procedures.

- Doctor Visits & Prescriptions: Coverage for routine visits and medication.

- Ancillary Benefits: Check for dental and vision care, as these are often included.

- Group Life Insurance: This is a lump-sum payment (often 1x or 2x your annual salary) paid to your beneficiaries if you pass away while employed.

Jagdish’s Insight: “Don’t just file your benefits booklet away. Treat it like a critical financial document. Take 30 minutes to read it and understand your coverage limits, deductibles, and co-payments. Knowledge is the first step to maximizing value.”

The Critical Gaps: Where Your Work Plan Can Fall Short

While employer-provided group health insurance in Trinidad is an excellent foundation, it’s designed to cover a broad group, not your specific individual needs. Here are the most common gaps you need to be aware of:

1. It’s Not Fully Portable (The “Golden Handcuffs”)

This is the single biggest limitation. In most cases, your group coverage is tied to your job. If you leave your company, get laid off, or decide to start your own business, that coverage disappears. You could be left uninsured, and if you’ve developed a health condition, getting new coverage can become more difficult and expensive. Understanding your rights when changing jobs is important. You can find general guidance on employment best practices from sources like the Ministry of Labour.https://www.molsed.gov.tt/

2. The Coverage Might Be Basic

Employer plans are built to a budget. The coverage limits for major procedures or the life insurance amount (e.g., 2x your salary) is rarely enough to cover a mortgage, replace your family’s income for a decade, and fund your children’s long-term education.

3. You Have No Control

Your employer, not you, controls the plan. They can change insurance providers, reduce benefits, or increase your contribution cost at the next renewal period. Your personal strategy, on the other hand, puts you in control.

4. It Changes Significantly at Retirement

Group benefits typically terminate or change drastically when you retire. While some great companies like Maritime may offer a modified continuation plan for retirees, these often come with significantly reduced benefits. Relying on this alone can leave you underinsured precisely when your healthcare needs are likely to increase.

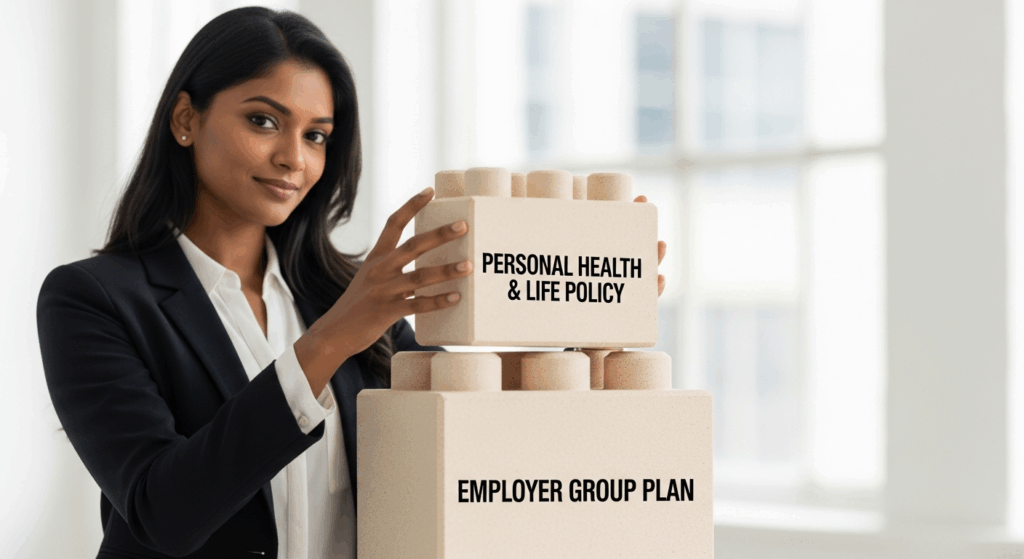

The Solution: A Personal Strategy for Group Health Insurance in Trinidad

A personal insurance strategy, designed by TrueHaven Advisory, doesn’t just replace your work benefits; it complements and completes them using smart, cost-effective solutions.

- Filling the Gaps with a “Small Group” Plan: At TrueHaven, we specialize in solutions like those from The Maritime Financial Group, which do not offer individual health plans but instead focus on “small group” plans. Micro and Small businesses or registered organizations can secure much lower premiums than a typical individual plan, making comprehensive coverage incredibly affordable.

- Flexible & Tailored to Your Budget: These plans are not one-size-fits-all. There are different tiers of coverage available to suit your specific budget and needs. You have the control to choose the level of protection you are comfortable with.

- Optional Life Insurance Add-on: To make things even more flexible, life insurance is often offered as a separate add-on to the health plan. This means you can purchase a powerful health insurance plan on its own, or you can bundle it with a life insurance component for complete family protection. You only pay for what you need.

- It’s Yours for Life: The plan you secure through us is completely portable. It stays with you no matter where you work, providing a continuous, reliable safety net that you can carry with you into retirement.

Conclusion: Build on Your Foundation with a Smarter Strategy

Your employer’s group health insurance in Trinidad is a valuable asset, and you should absolutely maximize it. But see it for what it is: a great foundation, not the entire fortress.” But see them for what they are: a great foundation, not the entire fortress.

To build true, lasting financial security, you need a personal strategy that fills the gaps with an affordable, flexible, and portable plan.

By leveraging “small group” plans, TrueHaven Advisory can design a solution that gives you premium coverage without the premium price tag.

Are you confident your current coverage is enough? Contact Jagdish Ramkissoon at TrueHaven Advisory for a free, no-obligation review of your employee benefits. We’ll help you understand what you have and show you how a personal strategy can build your ultimate financial ‘true haven.’

Call us at 678-4825 or visit https://truehavenadvisory.com