Introduction: The Armour You Didn’t Know You Were Missing

As a small business owner in Trinidad & Tobago, you are a special breed. You’re a risk-taker and the engine of our local economy. But are you truly protected? Getting the right business insurance is crucial, yet many entrepreneurs overlook the policies that shield them from devastating risks. In the day-to-day hustle of running a business, some critical aspects are overlooked. These aren’t luxury add-ons; but essential pieces of armour that can mean the difference between a temporary setback and a permanent closure.

At TrueHaven Advisory, we see brilliant entrepreneurs leave themselves dangerously exposed. Let’s review the three most commonly overlooked insurance policies and why ignoring them could be the costliest business decision you ever make.

1. Public Liability: A Must-Have for Small Business Insurance in Trinidad

What it is: Public Liability insurance protects your business against claims of injury to a third party ( customer, supplier, or a member of the public) or damage to their property that happens as a result of your business operations. Understanding your legal obligations is key. For more information on business best practices review reputable sources like the Trinidad and Tobago Chamber of Industry and Commerce.”https://chamber.org.tt/

The Overlooked Risk: Many small business owners, from food vendors to retail shopkeepers, think, “That would never happen to me.” However in our “sue-culture,” accidents happen, which can be financially devastating.

- The Trini Scenario: Imagine a customer slipping on a freshly mopped floor in your boutique. Or a contractor’s ladder accidentally falling and damaging a client’s expensive gate. Even a simple case of food poisoning alleged from your catering business. Without Public Liability, the legal fees and potential settlement would come directly out of your business’s pocket – or your own.

Why It’s Critical: One single liability claim, even a frivolous one, can wipe out years of hard-earned profit. This policy is your financial shield against the unpredictable nature of dealing with the public. It’s not just for big corporations; it’s essential for any business that interacts with people.

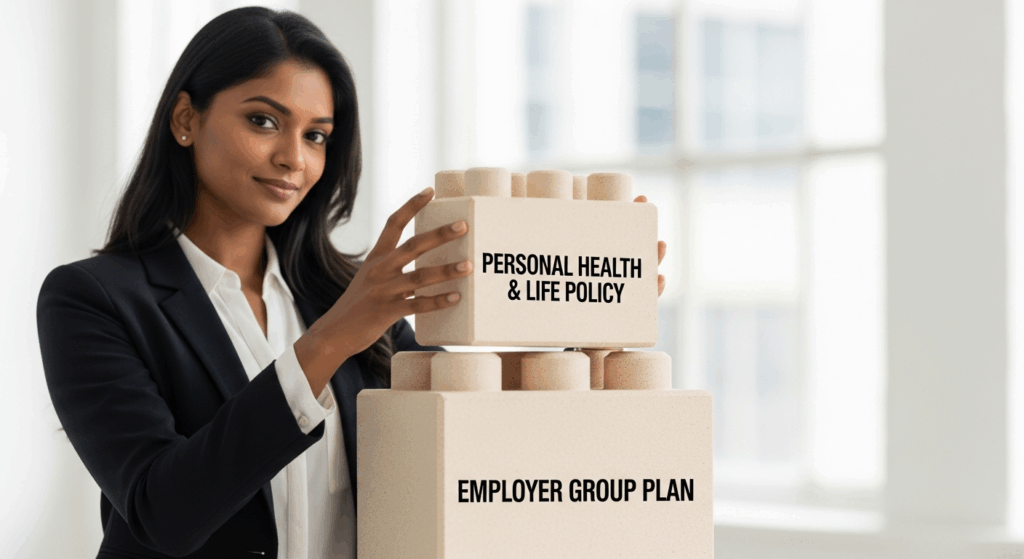

2. Group Life & Medical Insurance: The “Team Protector”

What it is: It is a policy that a business purchases to provide health and life insurance coverage for its eligible employees. It’s a cornerstone of a modern employee benefits package.

The Overlooked Risk: Many small business owners in T&T think of benefits as a “big company” luxury, not realizing it’s one of the most powerful tools for attracting and, more importantly, retaining top talent. In a competitive market, a good salary isn’t always enough.

- The Trini Scenario: You have a fantastic, highly-skilled technician or a brilliant administrative assistant who is the heart of your operation. A larger company offers them a better salary, but also a comprehensive health plan that covers their spouse and children. The peace of mind that comes with knowing their family’s health is secure is often the deciding factor that makes them leave. Losing that key employee can cost your business far more in lost productivity and recruitment costs than the group plan would have.

Why It’s Critical: Offering a group health and life plan is no longer just a perk; it’s a strategic business investment. It shows your employees you care about them and their families, which fosters loyalty and reducing costly employee turnover. Furthermore, it also ensures your team stays healthier and more productive. As the renowned entrepreneur Sir Richard Branson famously said, ‘Clients do not come first. Employees come first. If you take care of your employees, they will take care of the clients.’ A solid Group Life & Medical plan is one of the most tangible ways to show you are investing in your team.”

3. Key Person Insurance: The “Business Heartbeat” Protector

What it is: Key Person (or Key Man) insurance is a life insurance policy that businesses takes out on its most crucial individuals – the owner, a top salesperson, a uniquely skilled technician. The business is the beneficiary.

The Overlooked Risk: In many small businesses in T&T, the entire operation revolves around one or two key people. What happens if, you, the founder and chief strategist, were to become seriously ill or pass away unexpectedly?

- The Trini Scenario: A successful family-run restaurant where the head chef is the “brand” and the main reason customers come. If that chef is suddenly unable to work, the restaurant’s income could plummet. Key Person insurance provides the business with a cash infusion to manage the crisis. This money can be used to:

- Recruit and train a replacement.

- Pay off debts and reassure lenders.

- Provide a severance to employees if the business needs to close in an orderly fashion.

- Facilitate a buyout for the surviving partners or family members.

Why It’s Critical: This policy protects the business itself from the devastating financial impact of losing its most valuable asset, its key people. Ultimately, It’s about ensuring the business you’ve worked so hard to build has a chance to survive, even if you’re not there to run it.

Conclusion: Fortify Your Business, Secure Your Dream

Running a business takes courage. Protecting it with the right small business insurance in Trinidad takes wisdom. Don’t let your dream be derailed by a risk you didn’t see coming. These three policies—Public Liability, Business Interruption, and Key Person—are not expenses; they are critical investments in the resilience and longevity of your enterprise.

Is your business armour complete? Or are there gaps in your protection? Contact Jagdish Ramkissoon at TrueHaven Advisory for a complimentary, no-obligation Business Risk Assessment. Let’s ensure the business you’re building is protected for the long haul.